Calculations in conventional units. SCP

This article will cover the main cases of exchange rate differences, as well as how to reflect exchange rate differences in 1C 8.3.

According to clause 4 of PBU 3/2006, the value of assets and liabilities in foreign currency or cu. for display in accounting and reporting, it is recalculated into rubles. The difference in grade that arose as a result of this is called coursework.

According to clause 5 of PBU 3/2006, recalculation is carried out at the official exchange rate to the ruble, i.e. at the rate of the Central Bank of the Russian Federation or at another possible rate, if such a rate is established by agreement of the parties. Another rate by agreement of the parties may be, for example, USD + 1%.

Funds are subject to recalculation (in the bank, at the cash desk), as well as the value of the “debtor” and “creditor”* in foreign currency, which is carried out according to the following rules:

- By the date of receipt or write-off of DS in foreign currency/repayment of obligations;

- By reporting date, i.e. on the last day of the month.

*Advances issued and received in this structure are not subject to revaluation.

The difference resulting from the recalculation will be reflected in accounting as other income or expenses (depending on whether it is negative or positive) in 91 accounts. In the tax (profit tax) it is reflected as non-operating income or expense in the same account, but in the simplified tax system it will not be reflected.

Setting up accounting for exchange rate differences in 1C 8.3

To set up exchange rate differences in 1C 8.3, first of all you need to correctly set the details of the agreement with the counterparty. In this case we're talking about on contracts expressed in currency.

In 1C: Accounting 8.3, an agreement with a counterparty can be found using the “Agreements” link in the “Counterparties” directory element or in the “Agreements” directory. Both directories are located in the “Directories – Purchases and Sales” section.

Figure 1 – Section “Agreements” of the directory element “Counterparties”

Figure 2 – Directory “Contracts”

Let's consider two cases of concluding contracts in foreign currency.

If it is concluded with a resident, mutual settlements can only occur in rubles, because in accordance with the Law of December 10, 2003 No. 173-FZ “On Currency Regulation and Control,” currency transactions between residents are prohibited.

In the 1C 8.3 program, setting up an agreement with a resident expressed in currency will look like this. In the "Calculations" section for details "Price in" the currency value will be set, and the switch "Payment in" rubles will matter.

Figure 3 – Agreement settings with a resident

An agreement with a non-resident implies the possibility of mutual settlements in foreign currency, because in accordance with the Law of December 10, 2003 No. 173-FZ, non-cash currency transactions between residents and non-residents can be carried out without restrictions.

In the 1C 8.3 program, setting up an agreement with a non-resident expressed in currency will look like this. In the "Calculations" section for details "Price in" and switch "Payment in" the currency value will be set.

Figure 4 – Contract settings with non-residents

If the details are configured correctly and the downloaded courses are current*, all the data necessary for calculations will be filled in in 1C documents automatically.

*Rates can be loaded manually or automatically into the “Currency Rates” information register.

To manually download, open the “Currencies” directory in the “Directories/Bank and Cash Desk” section and click “Download exchange rates.”

Figure 5 – Directory “Currencies”

You can add a new currency to the directory using the “Create – New” button or select the required one from the classifier using the “Create – By Classifier” button.

Figure 6 – Adding currency from the classifier

For automatic loading, the settings of the scheduled task of the same name are performed.

Accounting for exchange rate differences in 1C 8.3

So, if the listed settings in the 1C program are made correctly, then the exchange rate difference is reflected automatically:

- By date of operation, through the document that registers this transaction. For example, through the documents “Receipt/write-off from current account”, “Sales/Receipt of goods”.

- At the end of the month through the “Revaluation of Currency Funds”, which is automatically launched in the “Month Closing” procedure.

Reflection of exchange rate differences in 1C 8.3

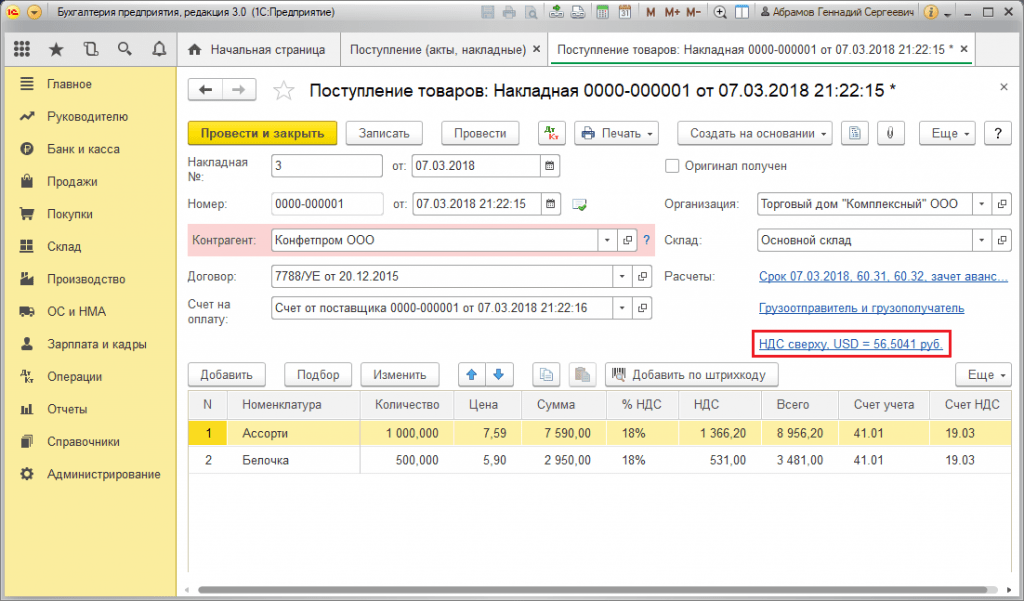

Example No. 1. In terms of purchasing goods under a contract in foreign currency

In our example, under the agreement with the supplier, the goods were shipped before payment. This event was recorded using the Goods Receipt document.

Figure 7 – Contract with supplier

Figure 7 – Contract with supplier

The rate in “Goods Receipt” was filled in automatically from the “Currency Rates” information register.

Figure 8 – “Receipt of goods”

Figure 8 – “Receipt of goods”

Figure 9 – Postings for “Receipt of goods”

Figure 9 – Postings for “Receipt of goods”

Payment occurred several days later than shipment and was registered in the program using the document “Write-off from account.” The currency rate in it was filled in automatically from the “Currency Rates” register, the “Amount” variable contains the value of the write-off amount in rubles, the “Settlement Amount” variable contains the value of the write-off amount in foreign currency. The exchange rate on the date of payment is filled in the “Settlement rate” detail.

Figure 10 – Document “Write-off from account”

Figure 10 – Document “Write-off from account”

The posting of the exchange rate difference in this case was reflected in the document “Write-off from the account”, because recalculation of the value of the creditor occurred on the date of repayment of obligations, i.e. on the date of payment.

The exchange rate difference is 702,752.79 - 706,446.64 = |-3,693.85| = 3,693.85 rubles. The resulting value coincides with the value in the posting for the exchange rate difference Dt 91.02 – Kt 60.31 in the document “Write-off from the current account”. Thus, the negative exchange rate difference was reflected in account 91.02 “Other expenses”.

Figure 11 – Postings according to the document “Write-off from account”

Figure 11 – Postings according to the document “Write-off from account”

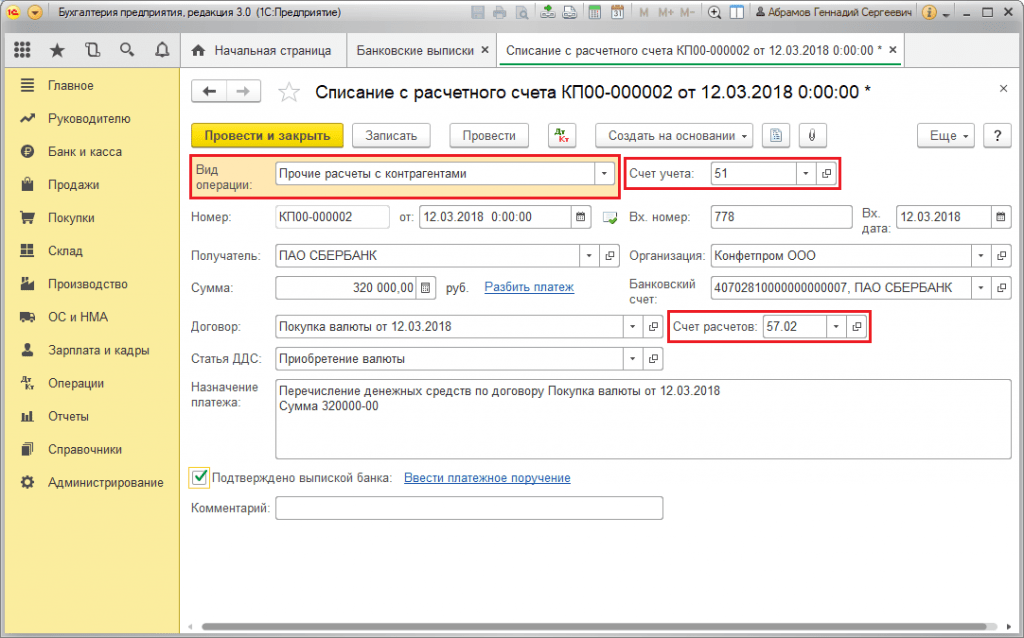

Example No. 2. In terms of currency trading

As part of the operation currency purchases transfer of DS to the bank is carried out through the document “Write-off from account” (type “Other settlements with counterparties”). The “Account Account” detail contains account 51 “Settlement Accounts”, and the “Settlement Account” – 57.02 “Purchase of Foreign Currency”.

Figure 12 – Enumeration Money to the bank for the purchase of currency from the document “Write-off from account”

Figure 12 – Enumeration Money to the bank for the purchase of currency from the document “Write-off from account”

Figure 13 – Postings “Write off from account”

Figure 13 – Postings “Write off from account”

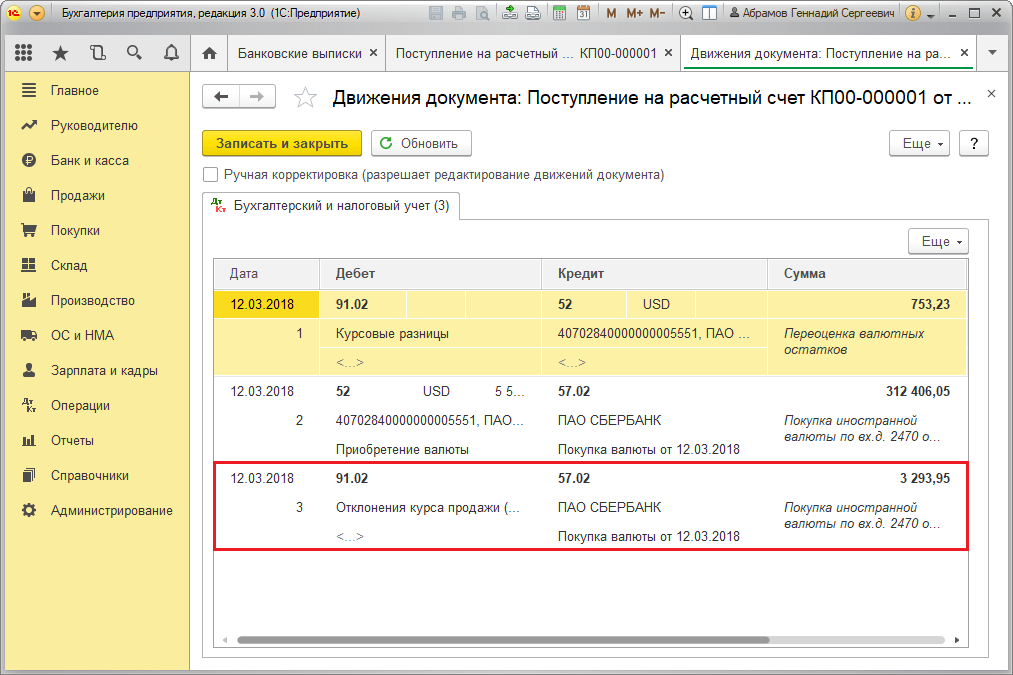

To credit the purchased currency to an account (respectively, a foreign currency account), it comes from “Receipts to the account” with the operational type “Purchase of foreign currency”. The line “Account” contains account 52 “Currency accounts”, and the “Settlements account” - 57.02 “Purchase of foreign currency”. “Bank rate” contains the exchange rate set by the bank for the purchase of currency. The Central Bank rate is filled in automatically in the details of the same name on the date of the operation. To display the difference, activate “Reflect exchange rate differences as expenses.”

Figure 14 – Crediting purchased currency to a foreign exchange account through “Receipt to account”

Figure 14 – Crediting purchased currency to a foreign exchange account through “Receipt to account”

DS in the amount of 312,406.05 rubles is credited at the Central Bank exchange rate and is reflected by entries Dt 52 - Kt 57.02 “Purchase of foreign currency”.

Here, the exchange rate difference occurs as a result of the recalculation of the DS on the date of receipt, so it is displayed in the “Receipt on account”.

The exchange rate difference is 312,406.05 - 315,700.00 = |-3,293.95| = 3,293.95 rubles. The resulting value coincides with the value in the posting for the exchange rate difference Dt 91.02 – Kt 57.02 in the document “Receipt to the current account”.

Thus, the negative exchange rate difference was reflected in account 91.02 “Other expenses”. Posting exchange rate differences in 1C:

Figure 15 – Posting for exchange rate differences when purchasing currency in the document “Receipt to account”

Figure 15 – Posting for exchange rate differences when purchasing currency in the document “Receipt to account”

The amount of 320,000.00 rubles transferred for the purchase of currency was more than 315,700.00 spent. Therefore, the balance of funds in the amount of 320,000.00 – 315,700.00 = 4,300 rubles must be credited to the ruble account through the document “Receipt to current account” with the transaction type “Other receipt”.

Operation currency sales carried out in a similar way:

- The transfer of funds to the bank from a foreign currency account is registered in “Write-off from account” with the view “Other settlements with counterparties”. The detail “Account” contains account 52 “Currency accounts”, “Settlement account” - 57.22 “Sales of foreign currency”.

- Crediting of DS from the sale of foreign currency to a ruble account is carried out through “Receipt to the current account” with the type of operation “Receipts from the sale of foreign currency”. “Accounting account” and “Settlement account” contain accounts 51 and 57.22, respectively.

Example No. 3. In conditions of recalculation on the final day of the month

As part of the routine operation “Revaluation of foreign currency”, the document is automatically launched in the “Month Closing” procedure, located in “Operations/Period Closing” or in “Operations/Period Closing/Routine Operations”.

Figure 16 – “Month Closing” procedure

Figure 16 – “Month Closing” procedure

When performing the routine operation “Revaluation of foreign currency”, the value of balances is translated into rubles for all accounts with the sign of currency accounting at the rate of the Central Bank of the Russian Federation in the directory “Currencies”. When revaluing foreign currency funds, the balance in foreign currency is considered unchanged.

Figure 17 – Transactions of currency revaluation

Figure 17 – Transactions of currency revaluation

Balances in the regulated accounting currency (rubles) are calculated at the rate indicated in the “Currencies” directory at the time of revaluation, therefore, before the operation, you should make sure that the current rates of the currencies used are established on the desired date of the reporting period (the final day of the month).

Since 01/01/2015, the concept of “amount difference” has been excluded from tax legislation Russian Federation. Deviations in amounts caused by changes in the foreign exchange rate established by the Central Bank or by agreement of the parties, when recalculating claims expressed in foreign currency and payable in rubles, are subject to the requirements of tax legislation established for exchange rate differences in Art. Art. 250, 265, 271 and 272 of the Tax Code of the Russian Federation.

In this article we detail simple example Let's consider how, from January 1, 2015, settlements with the buyer for goods supplied are reflected in the accounting records of the supplier organization, if the contractual value of the goods is established in foreign currency, and settlements are made in rubles. To demonstrate the above example, we will use the 1C: Accounting 8 edition 3.0 program.

According to Art. 506 of the Civil Code of the Russian Federation, under a supply agreement, a supplier-seller carrying out entrepreneurial activity, undertakes to transfer the goods produced or purchased by him to the buyer within a specified period or terms.

The buyer pays for the supplied goods in compliance with the procedure and form of payment provided for in the supply agreement (Clause 1, Article 516 of the Civil Code of the Russian Federation).

In accordance with paragraph 2 of Art. 317 of the Civil Code of the Russian Federation, a monetary obligation may provide that it is payable in rubles in an amount equivalent to a certain amount in foreign currency or conditional monetary units. In this case, the amount payable in rubles is determined at the official exchange rate of the relevant currency or conventional monetary units on the day of payment, unless a different rate or another date for its determination is established by law or by agreement of the parties.

Let's look at an example.

The organization "Rassvet" applies the general taxation regime - the accrual method and PBU 18/02 "Calculation of corporate income tax." The organization is a payer of value added tax.

On January 20, 2015, the Rassvet organization shipped goods to the Buyer organization. In accordance with the agreement, the price of the goods is set in foreign currency and is 1000 euros plus VAT 18% (180 euros).

Payment for the goods, in accordance with the contract, must be made in rubles at the official euro exchange rate on the day of payment plus 5%. The buyer paid for the goods on February 13, 2015. Euro exchange rates (conditional) on the date of shipment of goods, at the end of the month January and on the date of payment are presented in the table in Fig. 1.

Since the agreement of the parties defines a special (original) rate of payment for goods (euro + 5%), the first thing that needs to be done in the program is to create a new currency (conventional unit), which will be linked to the rate of another currency (euro).

To do this, you need to create a new element in the Currencies directory (we will call it “Euro + 5%”) and use the switch to indicate that it is associated with the rate of another currency - EUR, and the markup is 5%. An example of a created element in the Currencies directory is shown in Fig. 2.

Next, you need to correctly draw up an agreement with the buyer, let’s call it the UE Agreement. The type of contract, naturally, should be “With the buyer”, and in the Calculations section it is necessary to indicate that the prices in the contract are in currency (conventional unit) - EUR + 5%, and payment is in rubles.

An example of filling out the form for the Contracts directory element is shown in Fig. 3.

To perform the operation of shipping goods to the buyer, we will use the document Sales of goods and services with the Goods operation.

In the header of the document, we will indicate the counterparty-buyer and select the Agreement we have formed in the UE. In the upper right part of the document, in the Prices link in the document, the currency used in accordance with the agreement (EUR + 5%) and its exchange rate on the date of sale will be reflected. In accordance with our example, the rate of a conventional unit (cu) is determined as the official euro rate plus 5%: EUR rate + 5% = 74.00 rubles. * 105% = 77.70 rub.

In the tabular part of the document we will indicate the product being sold, its quantity and cost. In accordance with the contract, the cost of the goods is 1000 USD. (euro + 5%) plus VAT 18% (180 USD).

When carried out, the document will write off the goods sold (Dt 90.02.1 “Cost of sales for activities with the main tax system” - Kt 41.01 “Goods in warehouses”), accrue the buyer’s debt and recognize revenue (Dt 62.31 “Settlements with buyers and customers (in y. e.)" - Kt 90.01.1 "Revenue from activities with the basic taxation system") and will charge VAT (Dt 90.03 "Value Added Tax" - Kt 68.02 "Value Added Tax"). The document will also create an entry in the sales book (Sales VAT accumulation register).

The document Sales of goods and services and the result of its implementation are presented in Fig. 4.

In accordance with the presented transactions, the buyer's debt in rubles at the time of shipment is 91,686 rubles. (1180 cu * 77.70 rub.) in accounting and tax accounting.

The accrued VAT amount is RUB 13,986.

The seller is required to issue an invoice. The document Invoice issued is created in the usual way, using a link in the footer of the implementation document.

The printed form of the Invoice document issued is shown in Fig. 5.

The tax base for VAT on the sale of goods is determined at the time of shipment as the contractual value of these goods excluding VAT (clause 1 of Article 154 of the Tax Code of the Russian Federation).

In accordance with paragraph 4 of Art. 153 of the Tax Code of the Russian Federation, if when selling goods (work, services), property rights under contracts, the obligation to pay for which is provided in rubles in an amount equivalent to a certain amount in foreign currency or conventional monetary units, the moment of determining the tax base is the day of shipment, when determining tax base, foreign currency or conventional monetary units are converted into rubles at the official exchange rate on the date of shipment. Upon subsequent payment, the tax base is not adjusted. Differences in the amount of VAT incurred by the seller upon subsequent payment for goods are taken into account as part of non-operating income or non-operating expenses in accordance with Art. 250 and art. 265 Tax Code of the Russian Federation.

In accounting, the recalculation of debt expressed in foreign currency and conventional units, in accordance with clause 7 and clause 8 of PBU 3/2006, is carried out on the date of the transaction in foreign currency (payment date) and the reporting date (end of the month).

When recalculating the value of liabilities, the exchange rate difference is reflected in accounting (clause 11 of PBU 3/2006). The exchange rate difference must be credited to financial results organizations as other income or other expenses (clause 13 of PBU 3/2006).

For income tax purposes on transactions concluded from January 1, 2015, settlements in conventional units, as well as settlements in foreign currency, are revalued on the date of the currency transaction and on the last day of the month (clause 8 of article 271, clause 10, Article 272 of the Tax Code of the Russian Federation). When revaluing liabilities, the value of which is expressed in foreign currency or conventional monetary units, non-operating income or non-operating expenses are recognized - exchange rate differences (clause 11 of Article 250, subclause 5 of clause 1 of Article 265 of the Tax Code of the Russian Federation).

Posting of the routine transaction Revaluation of foreign currency at the close of the month January is presented in Fig. 6.

More detailed information on the revaluation of foreign currency can be obtained from the corresponding calculation certificate. When setting up this certificate, we will indicate that we want to receive accounting and tax accounting taking into account permanent and temporary differences.

From the certificate we see that the buyer’s debt is 1180 cu, the exchange rate of a conventional unit as of January 31, 2015 is equal to 81.90 rubles. (EUR rate + 5% = 78.00 rubles * 105%), the amount of debt in rubles before revaluation is equal to 91,686 rubles. The euro exchange rate has increased since the goods were shipped, the debt in rubles after revaluation is 96,642 rubles. (1180 cu * 81.90 rub.). The amount of debt in rubles as a result of revaluation increased by 4956 rubles. (96,642 rubles - 91,686 rubles), therefore, other income is recognized in accounting, and for income tax purposes, non-operating income in the amount of 4,956 rubles is recognized.

The reference calculation for the revaluation of foreign currency assets is shown in Fig. 7.

Payment for goods was made on February 13, 2015. Currency rate on this date is 78.75 rubles. (rate EUR + 5% = 75.00 rubles * 105%), therefore, in accordance with the agreement, the buyer transfers 92,925 rubles. (1180 cu * 78.75 rub.).

As we have already noted, in accounting since 2015, for income tax purposes, the recalculation of debt expressed in conventional units is carried out on the date of the transaction (in our case, the date of payment).

To reflect the transaction of payment of debt by the buyer, the program uses the document Receipt to the current account with the transaction type Payment from the buyer.

The header of the document indicates the payer-buyer and the amount of funds transferred by him.

In the tabular part of the document, select the agreement in accordance with which the payment was made. Debt repayment can be set either Automatically or By document. All other details in the table section will be filled in automatically.

When carried out, the document will revaluate the debt in conventional units in accounting and tax accounting, close the debt and capitalize the funds.

The document Receipt to the current account and the result of its implementation are presented in Fig. 8.

The buyer's debt is 1180 cu, the exchange rate of a conventional unit as of the date of the last revaluation (January 31, 2015) was 81.90 rubles. (EUR rate + 5% = 78.00 rubles * 105%), the amount of debt in rubles was 96,642 rubles. At the time of payment, the euro exchange rate dropped to 75.00 rubles. Accordingly, the rate of our conventional unit decreased - 78.75 (rate EUR + 5% = 75.00 rubles * 105%). The amount of debt in rubles on the date of payment is 92,925 rubles. (1180 cu * 78.75 rub.). As a result of revaluation, the amount of debt in rubles decreased by 3,717 rubles. (96,642 rubles - 92,925 rubles), therefore, other expenses are recognized in accounting, and for income tax purposes, non-operating expenses in the amount of 3,717 rubles are recognized.

Let's check the closure of the debt account - 62.31. The Account balance sheet report is presented in Fig. 9.

Let's see how regulated reporting is completed.

In accordance with paragraphs. 11th century 250 of the Tax Code of the Russian Federation, a positive exchange rate difference relates to non-operating income and is reflected in line 100 of Appendix 1 to Sheet 02 of the Profit Tax Declaration.

In accordance with paragraphs. 5 p. 1 art. 265 of the Tax Code of the Russian Federation, negative exchange rate differences relate to non-operating expenses and are reflected in line 200 of Appendix 2 to Sheet 02 of the Profit Tax Declaration.

A fragment of the income tax declaration of the organization “Rassvet” for the first quarter of 2015 is presented in Fig. 10.

A fragment of the VAT Declaration of the organization “Rassvet” for the first quarter of 2015 is presented in Fig. eleven.

Quite often, when an accountant enters into an agreement for the purchase of goods, expressed in currency or in conventional units (cu), problems arise with the formation of their value and reflection in accounting.

This article will help you not to get lost in dates, rates, and the cost of registering goods when converted to ruble valuation. Let's consider:

- legislative aspects of the acquisition of goods under a contract in monetary units;

- an action diagram in 1C to reflect the purchase of goods under a contract in cu;

- practical examples that provide a logical chain and order of execution of 1C documents.

After studying the article, you will never be confused about how to capitalize goods under these “notorious” contracts expressed in monetary units.

Purchase of goods under contracts in monetary units: legislation

Accounting and tax accounting

Transactions in foreign currency Russian organizations are prohibited and are carried out only in Russian rubles (Article 9 of the Federal Law of December 10, 2003 N 173-FZ).

In this case, the price in the contract can be expressed in any currency or conventional units (cu), other than rubles (clause 2 of Article 317 of the Civil Code of the Russian Federation).

Payment under such agreements must be made only in rubles at the rate agreed upon by the parties. As a rule, the agreed rate is equal to the rate of the Central Bank of the Russian Federation established on the day of payment. But often contracts may establish a different rate corresponding to the rate of the Central Bank of the Russian Federation plus 2%, minus 0.5%, etc.

Primary documents under such agreements can be presented in rubles, foreign currency or conventional units.

The value of assets (including goods) expressed in monetary units is subject to conversion into rubles in the accounting system (clause 4 of PBU 3/2006, clause 10 of Article 272 of the Tax Code of the Russian Federation).

The conversion rate depends on how payment for the purchased goods was made.

Goods for which payment was made in the form of 100% prepayment are recognized in the accounting system in ruble valuation at the rate in effect on the date of prepayment (paragraph 2, clause 9 of PBU 3/2006, clause 10 of article 272 of the Tax Code of the Russian Federation).

Goods for which payment is made after they are registered are recognized in rubles at the rate in effect on the date of transfer of ownership (clause 5 of PBU 3/2006, clause 10 of Article 272 of the Tax Code of the Russian Federation).

With a mixed form of payment in the form of partial prepayment and postpayment, goods are invoiced at the total cost:

- the paid part is assessed according to the date of prepayment (paragraph 2, clause 9 of PBU 3/2006);

- the unpaid portion is assessed at the exchange rate on the date the goods were accepted for accounting (clause 5 of PBU 3/2006).

At the same time, revaluation of accounts payable to suppliers under contracts in monetary units. should be carried out on the earliest date (clause 7 PBU 3/2006, clause 8 article 271 of the Tax Code of the Russian Federation):

- date of repayment of obligations;

- last day of the month.

In this case, exchange rate differences will arise, which are taken into account in account 91 “Other income and expenses”:

- in accounting - as other income or expenses (clause 13 of PBU 3/2006);

- in tax accounting - as non-operating income and expenses (clause 11 of article 250 of the Tax Code of the Russian Federation and clause 5 of clause 1 of article 265 of the Tax Code of the Russian Federation).

Find out more about Exchange differences.

VAT

The tax base for VAT is determined as of the earliest date (clause 1 of Article 167 of the Tax Code of the Russian Federation):

- day of shipment;

- payment day.

If the initial moment of determining the tax base under the agreement in c.u. is the day of shipment, it should be determined based on the exchange rate of the Central Bank of the Russian Federation on the day of shipment.

When subsequently paying for goods, VAT deductions are not adjusted. Differences in the amount of tax as a result of postpayment from the buyer are taken into account as part of non-operating income or expenses (paragraph 5, paragraph 1, article 172 of the Tax Code of the Russian Federation).

When purchasing goods, VAT is deductible (clause 2 of Article 171 of the Tax Code of the Russian Federation) if the following conditions are met:

- the goods must be used in activities subject to VAT;

- a correctly executed SF (UPD) is available;

- goods are accepted for registration (clause 1 of article 172 of the Tax Code of the Russian Federation).

The buyer has the right to deduct the amount of VAT indicated on the invoice. But you need to be careful and check the amounts of VAT in the Federation Council indicated by the supplier.

Invoices (UPD) for contracts in cu. are exhibited only in rubles. The ruble amount in the invoice for shipment depends on the payment procedure under the contract in cu.

Option #1. 100% prepayment according to the contract

The supplier is obliged to issue the shipping SF in ruble valuation at the rate of the Central Bank of the Russian Federation in effect on the date of prepayment (clause 14 of Article 167 of the Tax Code of the Russian Federation, Letter of the Ministry of Finance of the Russian Federation dated December 23, 2015 N 03-07-11/75467).

If an advance invoice was previously received from the supplier, then according to this invoice we also have the right to deduct VAT. But at the time of receipt of goods, VAT on the advance SF must be restored.

Option #2. 100% post-payment according to the contract

The supplier is obliged to set the shipping invoice in rubles at the rate of the Central Bank of the Russian Federation in effect on the date of shipment (clause 4 of article 153 of the Tax Code of the Russian Federation).

Option #3. Partial prepayment and postpayment according to the agreement

The supplier is obliged to set the shipping invoice in rubles at a cost consisting of:

- the paid part, assessed at the exchange rate on the date of prepayment (clause 14 of article 167 of the Tax Code of the Russian Federation);

- the unpaid portion, assessed at the exchange rate on the date of shipment (clause 4 of Article 153 of the Tax Code of the Russian Federation, Letter of the Ministry of Finance of the Russian Federation dated December 23, 2015 N 03-07-11/75467).

If an advance invoice for partial prepayment was previously received from the supplier, then according to this SF VAT we also have the right to deduct. But at the time of receipt of goods, VAT on the advance SF must be restored.

Purchase of goods under contracts in monetary units: accounting in 1C

Setting up functionality for accounting for contracts in monetary units.

In order for the 1C program to make it possible to keep records of contracts in monetary units, it is necessary to Currency directory enter several currency positions.

Drawing up an agreement in USD

If mutual settlements with the supplier are carried out under an agreement (invoice for payment), expressed in currency or cu, and payment is made in rubles, then when entering the agreement in the Contracts directory, it is necessary in the section Calculations indicate:

- Price in— currency or agreed rate specified in the contract;

- Payment in— checkbox rub.

Accounts of settlements with suppliers under contracts in monetary units.

When choosing a contract in USD To conduct mutual settlements with suppliers, settlement accounts intended in 1C for contracts in monetary units will be automatically established in the documents:

- 60.31 “Settlements with suppliers and contractors (in monetary units)”;

- 60.32 “Settlements for advances issued (in cu).”

As a result of posting documents, postings will be made to the corresponding accounts for mutual settlements with suppliers.

Exchange rate for currency conversion in rubles

Another feature of filling out documents under contracts in cu. is that when goods are posted in the document Receipts (acts, invoices) the tabular part indicates the cost of received goods in monetary units.

Accounting is kept in rubles and the cost of objects expressed in foreign currency is subject to conversion into rubles (Article 12 of the Federal Law of December 6, 2011 N 402-FZ).

The rate used by 1C for converting currency units. in rubles, is inextricably linked with rates in Currency directory.

The exchange rate or cu defined in the agreement is added to the directory. These can be rates of official currencies EUR, USD, as well as other currency rates, for example, rates such as EUR + 2%, USD – 1%, etc.

At the same time, to automatically fill in other courses in the directory Currencies they must be linked to the official rates of the Central Bank of the Russian Federation.

The rate used for ruble valuation of the cost of purchased goods will differ and depend on the payment procedure under the contract.

Sometimes organizations need to buy or sell foreign currency. The situation can be many things. For example, you import or export goods, send employees on business trips abroad, repay a loan in foreign currency, etc.

Current legislation obliges organizations to revaluate currency balances into rubles at the established rate. If an exchange rate difference arises in a positive direction for you, it is reflected as other income in accounting and as non-operating income in NU. The amount of the negative difference is taken into account in the same way, only for expenses.

In this article, we will use an example to look at how currency conversion operations are carried out in 1C 8.3 and consider their transactions, namely the purchase and sale of currency.

Before you start working with currency, you need to configure the program.

In the event that a transfer between a foreign currency and ruble account takes more than a day, you will need to use an intermediate account.

From the "Main" section, go to.

In the window that opens, find the item called “Account 57 “Transfers in transit” is used when moving funds” and mark it with a flag. This add-on does not need to be enabled.

It is also recommended to check the installation of another add-in. In the "Administration" menu, select "Functionality". In the settings window that appears, open the “Calculations” tab and check whether the checkbox for “Calculations in foreign currency and monetary units” is checked. We already had it installed by default.

In the “Directories” section, select “Currencies”.

You will see a list of all currencies added to the program with their rates. In this form, click on the “Download exchange rates...” button.

The program will prompt you to select those foreign currencies for which you need to download rates. Select the checkboxes and click on the “Download and Close” button. The default is the current date, but it can be changed.

Now you can proceed directly to our example of selling and buying currency in 1C 8.3.

Sale of currency

Write-off of foreign currency

Let's consider an example when our organization needs to sell $7,000 to Sberbank for rubles. Initially created in 1C payment order and based on it. We will not consider the payment order itself, and will immediately move on to processing the write-off, since it is this order that makes the necessary transactions.

Specify “Other settlements with counterparties” as the type of transaction. The recipient in our case is Sberbank PJSC. We have already concluded an agreement with him with settlements in USD. It is selected in the card of this document. The picture below shows a card of this agreement.

We will also write off accounting account 52 (Currency accounts) and settlement account 57.22 (Sales of foreign currency). In addition, you must indicate your organization and bank account.

Let's review the document and look at its postings. You can see that not only the write-off itself was reflected, but also exchange rate differences.

If the currency has changed its value since the last currency transaction, a posting will be added to 1C for calculating the revaluation of currency balances (if revaluation is configured).

Receipt to the current account

After the bank receives $7,000, it will transfer it to us in ruble equivalent. The program takes into account the document.

The receipt is filled in automatically after unloading from the client bank. However, it is recommended to check the completed details, especially the account and amount.

The movements of this document are shown in the figure below.

Buying currency

In case of purchasing currency in 1C 8.3, you need to perform the same actions as in the previous example.

In this situation, the write-off will look like “Other settlements with the counterparty”. In transactions for the purchase of currency, instead of 57.22 there will be 57.02 (Purchase of foreign currency). Receipts to the account will have the form “Purchase of foreign currency”.

Ekaterina Kolesnikova,

State Advisor civil service RF 3rd class

Especially for Taxcom company

The practice of concluding contracts in conventional units (hereinafter - cu) when paying for goods, works, services in rubles is widespread in many areas and is no longer new to anyone. But, despite the familiarity of such operations, some points when calculating in monetary units they still call headache from an accountant. Thus, for VAT tax purposes, it is worth considering the accounting features when the contract price is established in foreign currency or conventional units, and payment is made in rubles at the rate of the Central Bank of the Russian Federation on the date of payment, and not on the date of shipment, or the price is determined at the rate agreed upon by the parties, and not at the rate of the Central Bank of the Russian Federation. Despite the fact that from January 1, 2015, the concept of “total differences” for profit tax purposes disappeared from the Tax Code, which was intended to bring accounting and tax accounting closer together and simplify the work of an accountant, we should not forget about the peculiarities of accounting for exchange rate differences when reflecting transactions in financial statements. .e.

About calculations in USD

The opportunity to provide in an agreement with a Russian counterparty the cost of goods, (work, services), expressed in conventional units, and not in the official currency of the Russian Federation, is presented in paragraph 2 of Article 317 of the Civil Code of the Russian Federation, according to which a monetary obligation may be subject to payment in rubles in the amount , equivalent to a certain amount in foreign currency or in conventional monetary units (ecus, “special drawing rights”, etc.). By general rule, the amount payable in rubles is determined at the official exchange rate of the Central Bank of the Russian Federation of the corresponding currency to which the conventional unit is linked on the day of payment, unless a different rate or another date for its determination is established by law or by agreement of the parties.

According to the practice established in office work, contracts with obligations in monetary units. usually provide the following payment options for goods, works, services:

- Cost in USD payable in rubles at the exchange rate of the Central Bank of the Russian Federation on the date of payment;

- Cost in USD payable in rubles at the exchange rate of the Central Bank of the Russian Federation on the date of shipment;

- Cost in USD shall be paid in rubles at the rate agreed upon by the parties and stipulated in the contract.

The agreement may provide for any exchange rate for converting obligations into rubles; the procedure for determining such an exchange rate is also determined only by the will of the parties to the agreement. No one can limit the freedom of contract in this regard, which is confirmed by the conclusions made in paragraphs. 12, 13 Information letter of the Presidium of the Supreme Arbitration Court of the Russian Federation dated November 4, 2002 No. 70.

However, with a free determination of the exchange rate and settlement procedure, the parties should not forget about the requirements of the Tax Code for the procedure for taxation of transactions denominated in foreign currency and monetary units. Particular attention should be paid to operations in monetary units. and the procedure for calculations when determining the tax base for VAT.

Calculations in USD and VAT

According to the Rules for filling out an invoice, approved by Decree of the Government of the Russian Federation dated December 26, 2011 No. 1137 “On the forms and rules for filling out (maintaining) documents used in calculations for value added tax,” and clarifications of the Ministry of Finance of Russia given in a letter dated July 6, 2012 No. 03-07-15/70, an invoice, if paid in rubles, must be issued in rubles, regardless of what currency (cu) the contract price is set in.

At the same time, for the convenience of calculations, you can enter additional indicators into the invoice by adding columns or lines with the cost of goods, works, services in monetary units. and the rate of conversion of cost into rubles. Such recommendations are given in letters of the Ministry of Finance of Russia dated June 16, 2014 No. 03-07-09/28664, dated April 10, 2013 No. 03-07-09/11863. If your organization is a participant in electronic document management, it will not be difficult for you to supplement the electronic invoice with all the necessary data using “free fields”. The new formats approved for the invoice, the universal transfer act, contain all the necessary details and meet the requirements established by the Decree of the Government of the Russian Federation of December 26, 2011 No. 1137 and Art. 169 of the Tax Code of the Russian Federation. The advantage of electronic interaction with counterparties is the fact that electronic document formats are flexible in their use due to the presence of free information fields in them, which the organization can fill out at its own discretion, which allows taking into account the specifics of the event being processed.

It is much faster to exchange electronic documents with counterparties than paper ones; they are convenient to store, search and present at the request of the Federal Tax Service. Find out the benefits for your company.

When determining the tax base for VAT at the time of payment (partial payment) for goods (work, services), the Tax Code does not provide for a specific rule for converting the exchange rate of conventional units into rubles. When receiving an advance, the exchange rate used by the parties to calculate the cost of goods (work, services) is not so important, since in accordance with clause 4 of Art. 164 of the Tax Code of the Russian Federation, VAT in any case must be calculated on the amount of funds actually received at the calculated rate of 18/118%. The cost of goods, work, services for which an advance payment has been received is not subsequently recalculated for VAT purposes. Thus, discrepancies between the contract rate and the rate of the Central Bank of the Russian Federation will not arise in the future if 100% prepayment took place in the supply of goods (works, services). It should be noted that this situation will greatly facilitate the accountant’s work, but in reality, full prepayment is not as common as we would like.

But when determining the tax base for VAT at the time of shipment, the situation looks different. Tax Code in paragraph 4 of Art. 153 expressly stipulates that if, when selling goods (works, services), the obligation to pay for which is provided in rubles in an amount equivalent to a certain amount in foreign currency, or conventional monetary units, the moment of determining the tax base is the day of shipment (transfer) of goods (works) , services), when determining the tax base, foreign currency or conventional monetary units are converted into rubles at the rate of the Central Bank of the Russian Federation on the date of shipment (transfer) of goods (performance of work, provision of services).

Thus, tax code does not provide for any freedom in the procedure for determining settlements in monetary units, including the use of a rate agreed upon by the parties that is different from the official rate of the Central Bank of the Russian Federation. The fact that the procedure for calculating VAT by the seller does not depend on the foreign currency exchange rate or the conventional unit established by the agreement is evidenced by letters from the Russian Ministry of Finance dated February 21. 2012 No. 03-07-11/51, dated 07/06/2012 No. 03-07-15/70.

At the same time, upon subsequent payment for goods (works, services), the VAT tax base is not adjusted. Differences in the amount of tax that arise for the taxpayer-seller upon subsequent payment for goods (work, services) are taken into account as part of non-operating income in accordance with Art. 250 of the Tax Code of the Russian Federation or as part of non-operating expenses in accordance with Art. 265 Tax Code of the Russian Federation.

Particularly difficult for an accountant are transactions involving the sale of goods (works, services), the cost of which is expressed in monetary units, and payment is set at an agreed rate, different from the official one, upon receipt of a partial advance payment. Indeed, when determining the tax base for VAT on the day of shipment of goods (performance of work, provision of services) on account of the previously received partial payment in rubles, the above norm of clause 4 of Art. 153 of the Tax Code of the Russian Federation should be applied only to the part of the cost of goods (work, services), expressed in foreign currency or in conventional monetary units, not paid by the buyer on the date of shipment of goods (work, services). Thus, part of the cost of goods (work, services) not paid by the buyer on the date of shipment of goods (work, services) must be recalculated into rubles at the rate of the Central Bank of the Russian Federation on the date of their shipment, and previously received partial payment in rubles cannot be recalculated. This opinion is expressed in letters of the Ministry of Finance of Russia dated December 23, 2015 No. 03-07-11/75467, dated June 22, 2015 No. 03-03-06/1/35865, Federal Tax Service of Russia dated July 21, 2015 No. ED-4-3/12813.

Calculations in USD and income tax

When applying the accrual method, income is recognized in the reporting (tax) period in which it occurred, regardless of the actual receipt of funds, other property (work, services) and (or) property rights (accrual method). In this case, revenue from the sale of goods is recognized as income from sales, based on the contractual value on the date of transfer of ownership of goods, work, services from the seller to the buyer, which is confirmed by the provisions of paragraphs. 1 clause 1 art. 248, pp. 1 and 2 tbsp. 249, paragraph 3 of Art. 271 Tax Code of the Russian Federation. Accordingly, proceeds from sales must be converted into rubles at the rate agreed upon by the parties to the agreement, even if such rate differs from the official rate established Central Bank Russian Federation on the date of transfer of ownership of goods, works, services.

Until 2015, there were two types of differences in tax accounting, the procedure for determining which was slightly different from each other, as follows:

- exchange rate differences arose during settlements in foreign currency, as a rule, with foreign counterparties;

- amount differences arose during settlements with Russian counterparties, when payment was made in rubles, and the payment amount was equated to the amount expressed in currency or conventional units.

Starting from January 1, 2015, the concept of “amount differences” disappeared from Chapter 25 of the Tax Code of the Russian Federation, which brought accounting and tax accounting closer together and made the work of an accountant somewhat easier. Now all differences that arise during calculations both in foreign currency and in rubles linked to a certain conventional unit are called exchange rates. When transitioning to a new procedure for accounting for such transactions, special provisions were introduced stipulating that income (expenses) in the form of amount differences arising for the taxpayer on transactions concluded before January 1, 2015 should be taken into account for profit tax purposes in the manner established before this date, i.e. according to the old order.

The difficulty here is caused by the concept of “transaction”, which is given to us in the transitional provisions. The Ministry of Finance of Russia did not fully clarify when in its numerous letters (dated May 14, 2015 No. 03-03-10/27647, dated May 18, 2015 No. 03-03-06/1/28283, dated May 19, 2015 No. 03- 03-06/2/28746, 03-03-06/1/28749, dated 05.21.2015 No. 03-03-06/1/29152, dated 05.25.2015 No. 03-03-06/1/29921, dated 28.05 .2015 No. 03-03-06/1/30847) noted that in accordance with Art. 153 of the Civil Code of the Russian Federation, transactions are recognized as the actions of citizens and legal entities aimed at establishing, changing or terminating civil rights and obligations. Thus, from the point of view of civil law relations, a transaction is both the conclusion of an agreement (the supplier has an obligation to supply the goods, and the buyer has the right to demand its delivery) and shipment (the supplier has the right to demand payment for the goods, and the buyer has the right to obligation to pay).

Thus, if your organization entered into an agreement or shipped goods (performed work, provided a service) before January 1, 2015, then the differences arising from such operations should be taken into account according to the old procedure in the form of total differences.

When concluding a contract and/or shipping after January 1, 2015, the resulting differences will already be recognized as exchange rates. At the same time, for accounting and tax accounting purposes, exchange rate differences are calculated in the same way and the procedure for their calculation has long been known to us. At the end of the month and upon termination of the obligation, positive exchange differences are included in accordance with clause 11 of Art. 250 of the Tax Code of the Russian Federation as part of non-operating income; negative exchange rate differences - in accordance with subparagraph. 5 p. 1 art. 265 of the Tax Code of the Russian Federation in non-operating expenses.